New product premiums are not new, Green Premiums are different

Some climate startups want to charge customers a Green Premium for scaling, instead of investors. Those aiming for existing markets cannot use this approach. Electric Hydrogen shows the path forward.

Background

Some business ideas only make sense at scale. Businesses that rely on delivery networks are one example. Amazon has rarely paid a dividend to shareholders since it went public in 1997, because it has continuously reinvested its profits into expanding its distribution network. Two-sided marketplaces are another example. Uber spent more than $23B (!!!) in 2018 and 2019 alone to subsidize its riders. It finally reached profitability this year, 14 years after its founding. The TV show Silicon Valley even dedicated an episode to this concept (YouTube link).

Tesla famously took a different approach to the high marginal cost of low volumes. The company initially aimed at the luxury market, which has higher profit margins. It built a strong brand, where buyers could feel that their purchase of a $100,000 Roadster gave them something more than just a vehicle. Subsidizing products with the help of investor money or aiming for the luxury market are two ways in which startups have tried to address the issue of higher upfront costs. As far as I can tell, charging customers a Green Premium is a new method, that is increasingly championed by many energy and climate thinkers.

Customers pay for scaling with the Green Premium

According to the Breakthrough Energy page dedicated to the subject, “The Green Premium is the additional cost of choosing a clean technology over one that emits more greenhouse gases.” The website explains that,

The average retail price of ground beef is $3.79 per pound, while a plant-based burger is $5.76 per pound. The Green Premium for a zero-carbon burger is the difference in cost between the two, or $1.97. But the regular burger doesn’t reflect the true cost of emissions generated in its production.

Any salesperson can tell you that people buy a new product over an incumbent if it’s i) better, ii) cheaper, or iii) lowers risk, and lowering risk has the same effect as lowering cost. Products that charge a Green Premium are by definition not cheaper. They also generally do not directly reduce risk for the buyer. Climate change is a significant risk, but that risk is borne by everyone, as emissions are an economic externality. The buyer cannot draw a direct line between their purchasing decision and their reduction of risk, the way that they can for buying a home security system. The only remaining solution is to convince the buyer that this greener product is better.

What constitutes a “better” product? Other than price, which was discussed earlier, products can be better on features or specifications. For example, you may decide to purchase a new cellphone because it has an ultra-wide angle lens, which was a missing feature on your previous phone. Alternatively, you may purchase a new phone because it has a faster processor than your previous one, which was poorer in this specification. This kind of product differentiation is key to building new markets or capturing underserved market segments.

“Lowering emissions” is a product feature

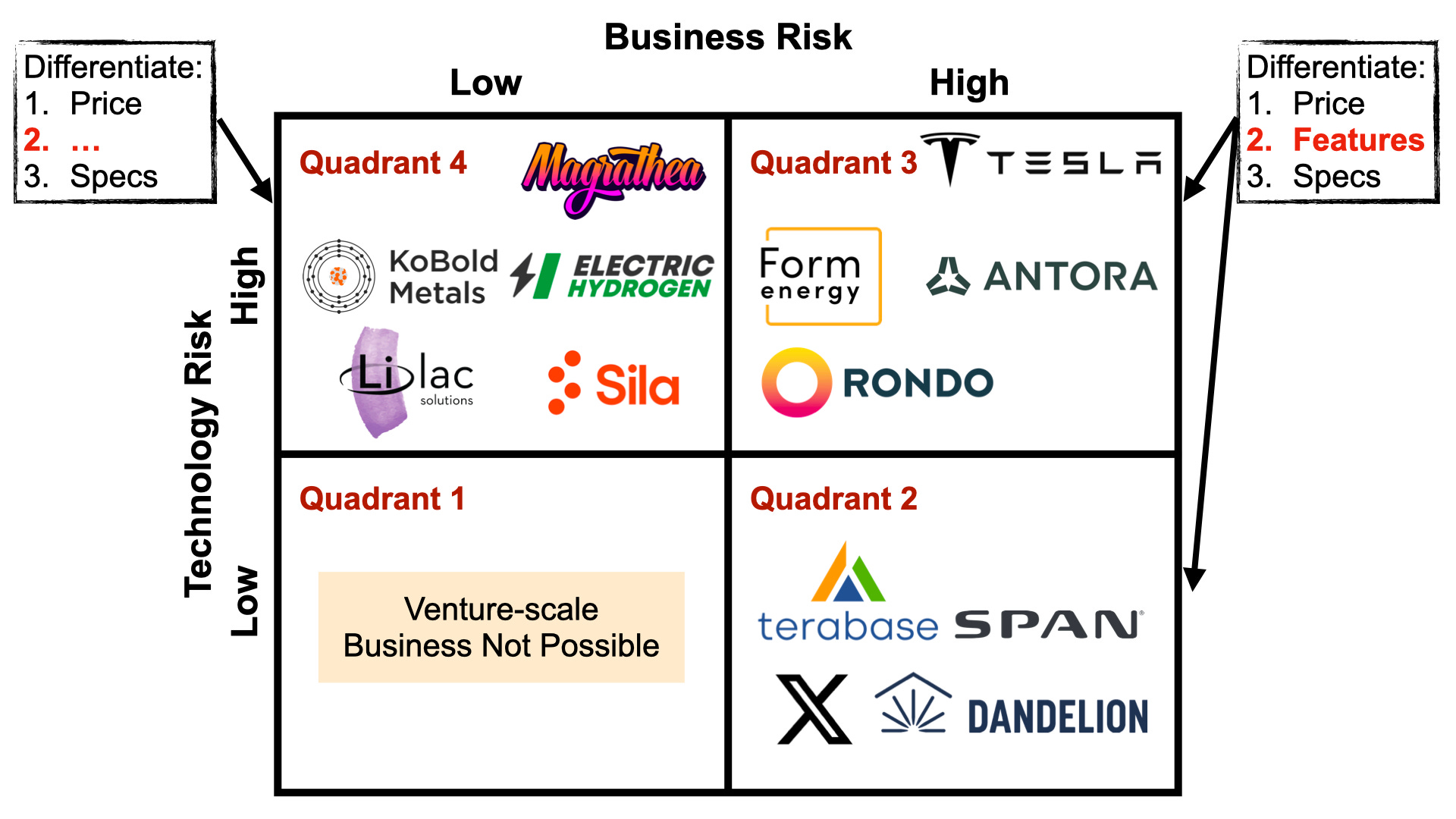

I have written before that startups with high business risk (quadrants 2 and 3) are creating new markets or product categories, whereas startups with low business risk (quadrant 4) are taking over existing markets (Fig. 1). Business risk is lower for quadrant 4 companies because there is never a question of what features to build. The product features in the market are already known, and the new entrant merely has to beat the incumbents on specifications or price. For example, the quadrant 4 company Sila Nano builds Titan Silicon™, which mimics graphite in battery anodes in every way, with the difference that it increases energy density by 20%. Sila’s product differentiation is on specifications, and it may even charge a higher price than the incumbents. Electric Hydrogen (EH2) is a quadrant 4 company helping to produce hydrogen from electrocatalysis instead of fossil fuels. Hydrogen is a commodity and an element on the periodic table, so there is no way to beat the incumbents on specifications. As I have written before, EH2’s main innovations are around ways to meet or beat the incumbents on price.

Lowering emissions is a product feature, and startups in quadrants 2 and 3 may be able to charge a Green Premium for this feature. Startups in quadrant 4 cannot differentiate their products based on features. Therefore, they cannot charge customers a Green Premium at scale. I have emphasized “customers” because these companies may be able to charge other entities such as the government a Green Premium in the form of incentives. I have emphasized “scale” because it may be possible to charge more for pilots or corporate initiatives, but not the level of output that impacts the day-to-day operations of most customers.

Branding commodities is ineffective

A few of the most famous climate tech categories (steel, cement, electrofuels, hydrogen, etc.) fall in quadrant 4, as large markets for these products already exist. Some startups active in these categories, which are mostly commodities, have created trademarked brands for their products to differentiate them as less carbon-intensive. They may be planning to use this branding as a way to charge customers a Green Premium. Firms that produce commodities are generally price-takers, which means that they “must accept prevailing prices in a market.”

Other commodity producers have tried branding their products as well, without much success. Chevron with Techron® and Shell V-Power® are gasoline brands based on the name of their proprietary engine-cleaning detergent fuel additives (Fig. 2). The content of gasoline, including the addition of detergents, is tightly regulated and controlled nationally. That fact may be why consumers are most likely to choose gas stations based on price (>70% for some surveys), and they have a much weaker association with gasoline brands (<35% for most surveys). This exercise reminds me of an episode of Mad Men, where Don Draper encourages the executives of the tobacco company Lucky Strikes to brand their cigarettes with “It’s Toasted.” One of the executives protests, “But everybody else’s tobacco is toasted.” Don clarifies, “No. Everybody else’s tobacco is poisonous. Lucky Strikes is toasted.”

Electric Hydrogen shows the path forward

The seasoned founder and CEO of a battery technology startup once told me, “The software business is all tactical. This business is all strategy. We started this company more than a decade ago. Right now I am not thinking about next year. I am thinking about five years from now.” In Good Strategy/Bad Strategy, Richard Rumelt notes that “The most basic idea of strategy is the application of strength against weakness. Or, if you prefer, strength applied to the most promising opportunity.”

Cleantech commodity startups have multiple strengths. As quadrant 4 companies, they are aiming for enormous existing markets like steel ($550B), cement ($420B), and hydrogen ($150B). The secular shift in the cost of electricity is another strength for these companies. Renewables like solar photovoltaics have reduced in price by an order of magnitude over the past decade, and they are now less expensive than fossil fuel alternatives (Fig. 3). These companies should be able to leverage such strengths and use investor funding to scale their operations, just as Uber did.

One of the reasons that I like Electric Hydrogen is that they have been applying these strengths to building an economical product. Raffi Garabedian, their co-founder and CEO, told the MCJ podcast,

Looking back at hydrogen over the years… we could never make ourselves convinced that hydrogen could be produced economically relative to the alternatives. And the alternatives are fossil resources. So, now fast forward to the end of 2020… and the situation had changed… Renewable electricity generation, both solar and wind, are now… cheaper than any other form of generation.

That's a key input to the production of renewable hydrogen. The missing link is … [a system that can perform] hydrogen conversion in a really cost-effective manner… Dave [our CTO] had a hypothesis… around how electrolysis can be driven in the same kind of way that we drove very successfully over the decades solar technology… By improving conversion efficiency you drive down the cost.

Electric Hydrogen is using the secular shift in electricity prices and the founders’ expertise in building efficient conversion systems to create a new and economically relevant source of hydrogen. Please note that capturing this market with such an approach only made sense at the end of 2020, when the price calculations finally made sense. It is bad to be too late, but also it is bad to be too early. In the same MCJ interview, Raffi makes it clear that his company makes economic sense regardless of any policy provisions.

It's all about economics. For this to be successful, it's got to be cheap. And what does cheap mean? It's got to be on par with the fossil resource. Now, we can sit around and wax on philosophically about, ‘Gee, wouldn't it be great if there were a carbon tax? Gee, wouldn't it be great if we could monetize… the societal costs of CO2 emissions?’ … We've been waiting for a long time. We finally have the technology, we believe at Electric Hydrogen, and the resource to achieve cost parity in the next few years with the fossil resource, without actually having to have all those other great policy things that could accelerate adoption even further.

Electric Hydrogen shows the path for building a cleantech commodity startup. The company does not expect its customers to fund its scaling efforts by paying a Green Premium. Instead, it is using less expensive inputs and a more efficient process to build a commodity that can compete with the fossil fuel alternative on price. The fundamental economics of the company make sense. That is why even in the absence of any policy initiatives it can use investor financing to scale.

Conclusion

The Green Premium is a way to charge customers for scaling costs, which have historically been borne by investors. Companies with high business risk may be able to charge a Green Premium for the product feature of “lowering emissions.” Companies with low business risk can only differentiate themselves on price or specifications, and cannot charge a premium for such a feature. Furthermore, branding commodities in this quadrant is an ineffective product differentiator. Companies with low business risk have the advantage of pursuing known and sizable markets. They should be able to scale using investor funding as long as they can show that secular trends and their technologies allow them to compete on price. Companies with low business risk may not have access to the Green Premium, but if they are set up properly they should not need it either.

A song I like

A scene I like

Cool Hand Luke: “Sometimes nothin’ can be a real cool hand.”

Great article. I agree that companies, especially startups, should not rely on policies for scaling up.